- Review: MariBank | Mari Business Loan (Credit Line) – Do I Need a Business Credit Line?

- Banks in Singapore - Do They Reimburse Losses from Scams and Fraud?

- Singapore Businesses’ Guide to Hiring Interns + Grants For Interns [2024 Updated]

- Understand the Basics of Credits and How to Avoid Getting into Bad Debt

- Comprehensive Guide to Data Protection Officer - What SME Owners Need to Know [Updated]

- How to avoid being a victim of credit frauds/scams?

- Why do employers conduct background screening?

- Corporate Compliance in Singapore: Guide for SMEs and Businesses

- Should I Switch My Corporate Secretary Partner?

- Comprehensive Guide to Understanding Moneylenders Credit Bureau (MLCB) Loan Information Report

Understanding Your Credit Report from Credit Bureau Singapore - Business Owner Edition 2023

Most business owners might need to take a Business Loan at least once in their lifetimes. However, you might not know that your ability to get one may be affected by something known as your credit score.

A credit score is derived from your credit report, which denotes your credit reputation and trustworthiness. If you have a high credit score, you are deemed to be less likely to default on a loan payment, which can improve the chances of your loan application being approved as well as the terms of the loan itself.

Considering how important getting a business term loan is in this COVID-19 situation, our credit score is of great significance in getting the loan approved. But how can you maintain or improve it?

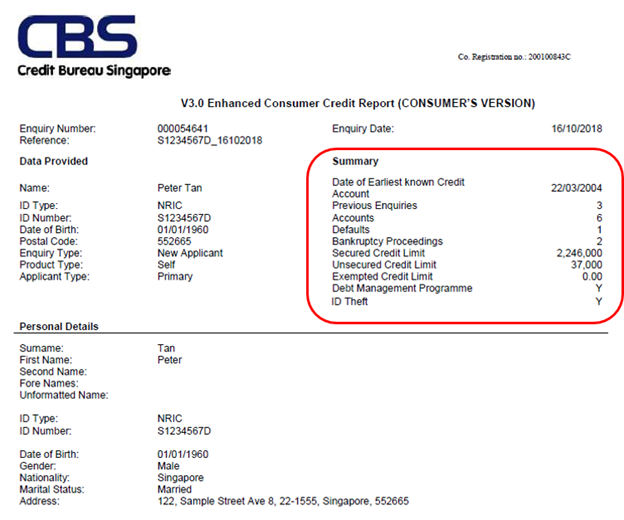

How to read your credit report

Your credit report is generated by Credit Bureau (Singapore) Pte Ltd (CBS), Singapore's only comprehensive consumer credit bureau that has 100% full-industry uploads from all retail banks and major financial institutions.

These data from banks are then supplemented with publicly available information such as bankruptcy and Debt Repayment Scheme records from the Insolvency and Public Trustee’s Office (IPTO) as well as Debt Management Programme information from Credit Counselling Singapore.

The information displayed in your credit report is encapsulated by your account summary, which details the number of bank accounts you have, the number of times that your credit file has been accessed and reviewed by lenders, your total credit limit across all banks in Singapore and any presence of default or bankruptcy records.

The report then goes on to include more comprehensive records, such as:

Personal details

Records of all enquiries made on the individual’s report, including self-enquiries, 2 years from the date of enquiry

Credit repayment trend for the past 12 months

Default records, if any. Default records with the status of Negotiated Settlement or Full Settlement will be displayed for 3 years from status date. For default records with the status of Outstanding, Partial Payment and Sold Off, the records will be displayed indefinitely on the report

Litigation records, if any

Bankruptcy records, retained for 5 years from the date of discharge

Closed or terminated credit accounts going back 3 years from the date the account was reported closed or terminated

Aggregated outstanding balances, computed based on the amounts outstanding under borrowers’ credit cards and credit facilities, including any fees and interest accrued thereon

Aggregated credit limits

Bureau or credit score, which is calculated from an algorithm based on information in your current available credit data and is a fluid number which may change from time to time in tandem with changes in your credit information

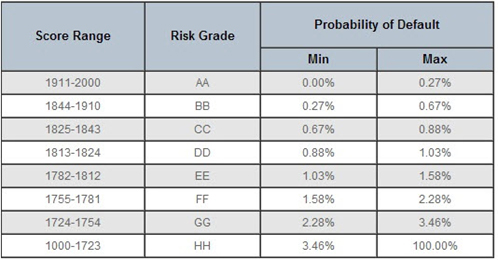

As explained, the credit score is a number used by lenders as an indicator of how likely an individual is to repay his debts and the probability of going into default. The score ranges from 1000 to 2000, upon which you will be given a risk grade from “AA” to “HH”.

Credit: creditbureau.com.sg/credit-score.html

Answer: Knowing the right Financial Institutions to approach is important, some banks / financial institutions will outright reject applicants that have GG credit rating regardless of company financial strength, while some Financial Institutions like Orix Leasing and Ethoz Capital do not run credit bureau check for companies that have more than one director / shareholder.

What Other Factors In My Credit Score Will Affect My Business Loan Application?

Banks look at the repayment conduct as reflected in the director's CBS.

Let us take a look at the example below:

What does First Row Mean?

Besides the above factors, banks also look at your Aggregated Outstanding Balances VS Total Credit Limit.

Total Unsecured Credit Card Limit

How to check your credit score in Singapore?

To check your credit score, you will have to obtain your credit report from CBS. You can request for a copy of your credit file online, at any of the SingPost branches, at the Credit Bureau office or at CrimsonLogic Service Bureaus.

The charges are as follows:

The CBS credit report itself costs S$6.42 (inclusive of GST).

If you request for multiple modes of delivery for your report, there will be an additional fee of S$2 charged for the service.

You may collect your report within 2 hours at any SingPost outlet for an additional administrative fee of S$17.12 for the express service.

Is your credit score good or bad?

Beyond the extreme ends of the spectrum where things are more obvious (a score in the range of risk grade AA is clearly good and HH is clearly bad), it can be difficult to tell. Different banks have different risk appetites at different times, hence their lending policies can differ. A credit score in risk grade BB might still not be enough for a credit facilities application to be approved.

The best thing you can do is to improve your credit score as much as you can, and keep it at that highest possible level.

How to improve credit score in Singapore?

The factors that affect your credit score are as follows:

Factors | Description |

Utilisation Pattern | The amount of credit amount owed/used on accounts by individuals. |

Recent Credit | Lenders may perceive that you are over-extending yourself if you have newly booked credit facilities within a short period of time. |

Account Delinquency Data | Presence of delinquency (late payment) on your loan accounts will reduce your credit score. |

Credit Account History | A consumer with long established credit history is deemed to be more favorable or a reliable borrower when compared to one who has limited or no credit history. |

Available Credit | This refers to the number of accounts available (open or active) for credit. |

Enquiry Activity | This refers to the number of new application enquiries found in your credit. |

As such, the ways to bring up your credit scores are:

Always repay loans on time, for obvious reasons. Even if your bank waives any late payment fees, you can be sure that late payments will still cause your credit score to fall.

Avoid making multiple loan enquiries in a short time, as having too many enquiries in your credit report indicate to lenders that you are trying to take on more debt, therefore increasing your credit exposure.

If you’re trying to find a business loan or mortgage loan, you may reach out to our friendly Smart Towkay team for advice!

Don’t have too many credit facilities open. Lenders may perceive that you are over-extending yourself if you are holding too many credit cards or credit lines.

Never default on your loans, as this will be shown on your credit report indefinitely, leaving an indelible mark on your reputation that can make it impossible to ever get a credit card, line of credit, or home loan again. If repayment really cannot be made, always seek credit counselling and have your debt restructured instead, as this will still lower your credit score but not permanently.

Take and repay a loan to repair damaged credit. This might be somewhat gaming the system, but taking a small short-term loan (even if you don't really need it) and repaying it fully on time will be taken into account by CBS and your credit score will improve.

What to do if you spot an error

It is not impossible for there to be mistakes in your credit data, which could affect your credit score. If you do notice a mistake, contact CBS and the bank or financial institution that originated the entry and get them to reverse or amend it.

It is a good habit to check your credit report periodically, or at least a few months before you anticipate that you might require credit facilities. This way, if there are errors that are adversely impacting your credit score, you have time to remedy them and to improve your credit score.

Read also: Complete Guide To Buying Commercial Property In Singapore

Read also: Income Tax 2021: Tax Deductions On Work From Home Expenses

Read also: 5 Ways to Build Business Credit in Singapore

Read also: Guide to Getting a Home Loan in 2021

-------------------------------------------------------------------------------------------------------

Got a Question?

WhatsApp Us, Our Friendly Team will get back to you asap :)

Share with us your thoughts by leaving a comment below!

Stay updated with the latest business news and help one another become Smarter Towkays. Subscribe to our Newsletter now!